Money Monies is hosted on wordpress.com on a free plan. I didn’t want to pay for anything before I get anywhere. Hence, the website comes with a lot of limitations. I have little control about what I can do. Nothing here belongs to me other than the content. After figuring out there is a free hosting service, I decided to make the move.

I can’t even redirect any URLs of this blog to my new website for free. WordPress wants to charge me USD 13 a year. Well… since this blog isn’t exactly the most popular thing out there, I think I can save a lot more money by moving.

2. Rebranding

I think Beans are cuter. hah hah.

Alright, see you on the other side! Twitter and Facebook page will remain for now.

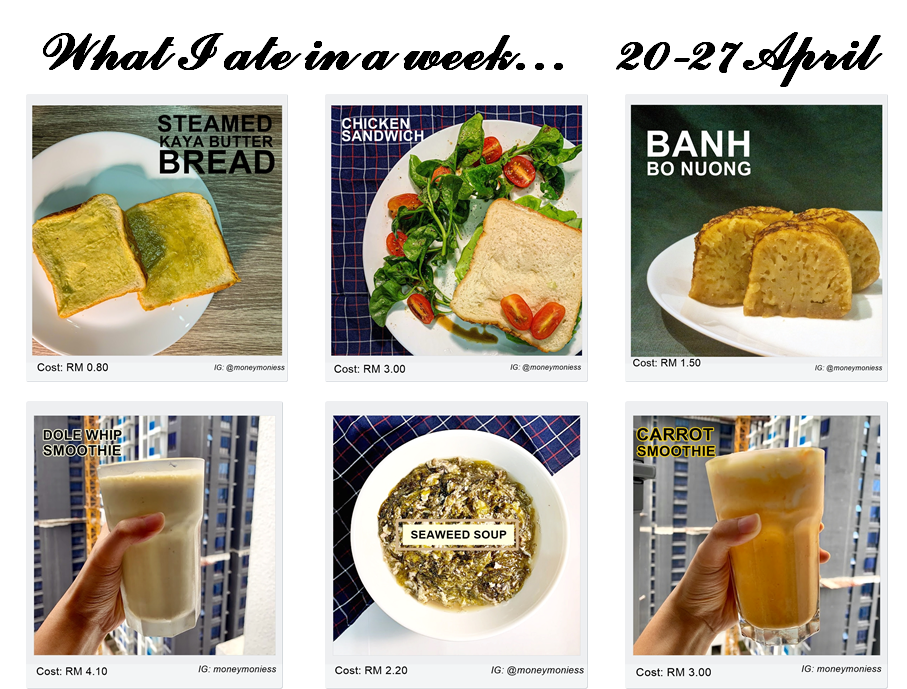

After reading Ringgit Oh Ringgit’s post on Personal Finance Blog Ideas, I have decided to update on my food spending for the week! (It is also fortunate that I kept the receipts this time around.) Here goes, my meals for the week and how much they cost, and some pictures.

Where do you shop for groceries?

Living a car-free life in Kuala Lumpur means I have extremely limited choices of grocers around me, i.e. I can’t go to the wet market, or head to the cheaper ones. I make do with what I have. There are two grocers around me and the nearest one would be Village Grocer. While people associate Village Grocer with high prices, I think their fresh (vegetables etc.) prices are fair, and they are as fresh as the name. For meat, prices are on the higher end, and fortunately or not, I am mostly a vegetarian.

How do you plan your grocery shopping?

To give you some ideas about how I plan my grocery shopping for the week, there are several considerations.

Price –The first section I check out is always the ‘Reduced Price’ section. I will check out what is available and plan my meals around it. I will also check out what products are on offer and purchase those.

Longevity of the ingredients – I take stock of what I bought and prioritize cooking those that wouldn’t last long.

Rough recipes in mind – Sometimes, I head to the grocers with particular recipes in mind. Maybe it is palak paneer, dumplings, cake, etc.

Honestly, I used to eat a lot more when I was weight lifting. I can’t go to a workout hungry, hence I wasn’t able to practice intermittent fasting for a while. Recently, due to the closure of gyms as a result of the MCO, I am mostly doing yoga and low intensity workouts.

My ingestion period is between 12pm to 6pm, and in the morning I have only black (instant) coffee. There are of course times I break the fast past 6pm (life is hard especially if you love food shows), but I will try to limit the snacking to low calorie stuff like seaweed.

So, show us the meal plan!

Honestly, I am really proud of some of the pictures. Check out my instagram for more!

The Detailed List:

The total cost for the week come to be: RM 122.50.

As you can see, there are a lot of repeats in the list. Most of the time, I would just cook for one round and have the food for a few days. You can also see that I eat a mostly vegetarian diet. There is very little meat in my diet.

I also took the chance to assess my eating habit. I think you will be able to tell I have a sweet tooth (demonstrated by the highlights). My packaged food consumption is limited and I would like to keep it that way. I only ordered delivery once, good job to myself! You can see how the delivery blows the budget out of proportion.

RM122.50 for a week’s of food spending in Kuala Lumpur. Is it surprising? Some of my (frugal) friends in UK/USA can keep their monthly food budget to be around £100 / $125. I am spending about the same amount as them in absolute currency terms (~ RM500), but the percentage of food to income is a lot larger. While people talk about how cheap food in Malaysia is, on a relative scale, it is actually rather expensive. While food costs about the same in developed countries in absolute terms, people make a lot more.

Should I cut my budget for food further?

I do think I can trim my food cost further if I do it ERE style and eat lentils all week, but for now, I would be happy if I can keep this spending level.

I am also sharing the calculations and recipes below.

Expand to see!

Nescafe Gold – RM21/packet from Shopee, one pack typically lasts about 3 months. I drink it daily.

Cream Spinach and Scrambled Eggs – 3x eggs (RM 1.30), 50g of Brazilian Spinach (RM 0.90), Cream (RM1.50)

Banh Bo – 7x Eggs (RM 3.00), 400ml of Coconut Milk (RM 4.20, 1l of coconut milk is RM10.90), 320g Tapioca Flour (RM 0.40), 80g Rice Flour (RM 0.30), 300g Sugar (RM 0.90), Pandan Leaves (RM 0.40)

Steamed Butter Kaya Bread – 2x of Gardenia Bread (RM 0.50), Kaya (RM 0.15), Butter (RM 0.15)

Baked Bell Pepper and Cucumber – Bell Pepper (RM 2.20), Cucumber (RM 4.00)

This is the holy grail jacket. I’m never going to need to buy one again.

A friend

Yeah, but it’ll last longer.

Me, justifying why I need a really expensive bag to my girlfriend

I just realized I own $500 of underwear…

Another friend

Being frugal means you generally buy cheap stuff, but sometimes you go off and do a cost-benefit analysis on something more expensive and figure you’re willing to pay a premium for quality, comfort, and/or life-expectancy. A good example is high quality underwear. Once you catch a whiff of the experience of wearing any of the Internet’s favorite premium briefs, you might find it hard to go back to the cheap-o multi-packs Mom used to buy you from Walmart and Bob’s Discount Clothing.

Here’s an example (inspired by true events):

Let’s say you want to own 10 pairs of briefs, and compare the costs of cheap-o briefs with those of Premium Brand A. Using example prices from the table below, you calculate that the premium you will pay is $120. You find this cost-benefit reasonable, and you’re able to justify it further by amortizing the cost across the 5-10 years that you expect briefs to last, so you go ahead and decide to buy a set of premium briefs.

Cheap-o

Premium Brand A

Price per pair

$3

$15

Price for 10 pairs

$30

$150

This was a reasonable, controlled, and intentional use of your money. You looked at the costs, amortized them over time, thought about quality and comfort, and made a well thought out decision to purchase premium undies. Huzzah! You now don’t have to make decisions about underwear for the next 5-10 years.

A few months later, you catch a whiff of some internet talk about a new premium brand. Premium Brand B. Curious, you Google “Premium Brand A” vs. “Premium Brand B”. Just curious, you say to yourself. You find that the Internet has decided Premium Brand B is better than Premium Brand A. Ah well, you say to yourself. You were just curious, anyway. You’ve got underwear already. You don’t need to upgrade. But I wonder how they feel. So, you decide to order just one. Just curious, you again say to yourself. You’re not going to overhaul your underwear setup, you just want to give these new ones a try.

A week later, Premium Brand B briefs arrive at your door. You give them a try and compare. Lo and behold, the internet was wrong: Premium Brand B unquestionably is not better than your good ole’ Premium Brand A. You spent an extra $15 on this experiment, but you can always use an extra, you suppose.

Two years later, a popular media site posts a huge comparison of 15 different premium briefs. Your trusty Premium Brand A does well, but Premium Brand C comes out on top. Like you did with Premium Brand B, you buy one, just to try. And voila, this time, the internet was right: Premium Brand C clearly is better than your good ole’ Premium Brand A.

At this point, you’re now in a small bind. You have a set of Premium Brand A briefs that was supposed to be your go-to for the next decade. You don’t really need an upgrade, and maybe you can easily shrug off Premium Brand C. On the other hand, maybe you think about living with Premium Brand A for 10 years, knowing all the while that there was something better. Maybe that nags you for a while. So, you do it. You wait for a decent sale, and you upgrade your set. Another $150. But at least now you won’t live for 10 years thinking what could’ve been.

So where are you now? $150 for your initial set of Premium Brand A briefs. $15 to try Premium Brand B. Another $150 to upgrade your set to Premium Brand C. You now have $315 of underwear.

It’s not hard for this sort of thing to repeat itself. It’s too easy to ditch the 5-10 year plan again, for yet another holy grail pair of underpants that eventually comes into the fray. And if you’re not careful, you may reach a point where you one day wake up and say “I just realized I own $500 of underwear.”

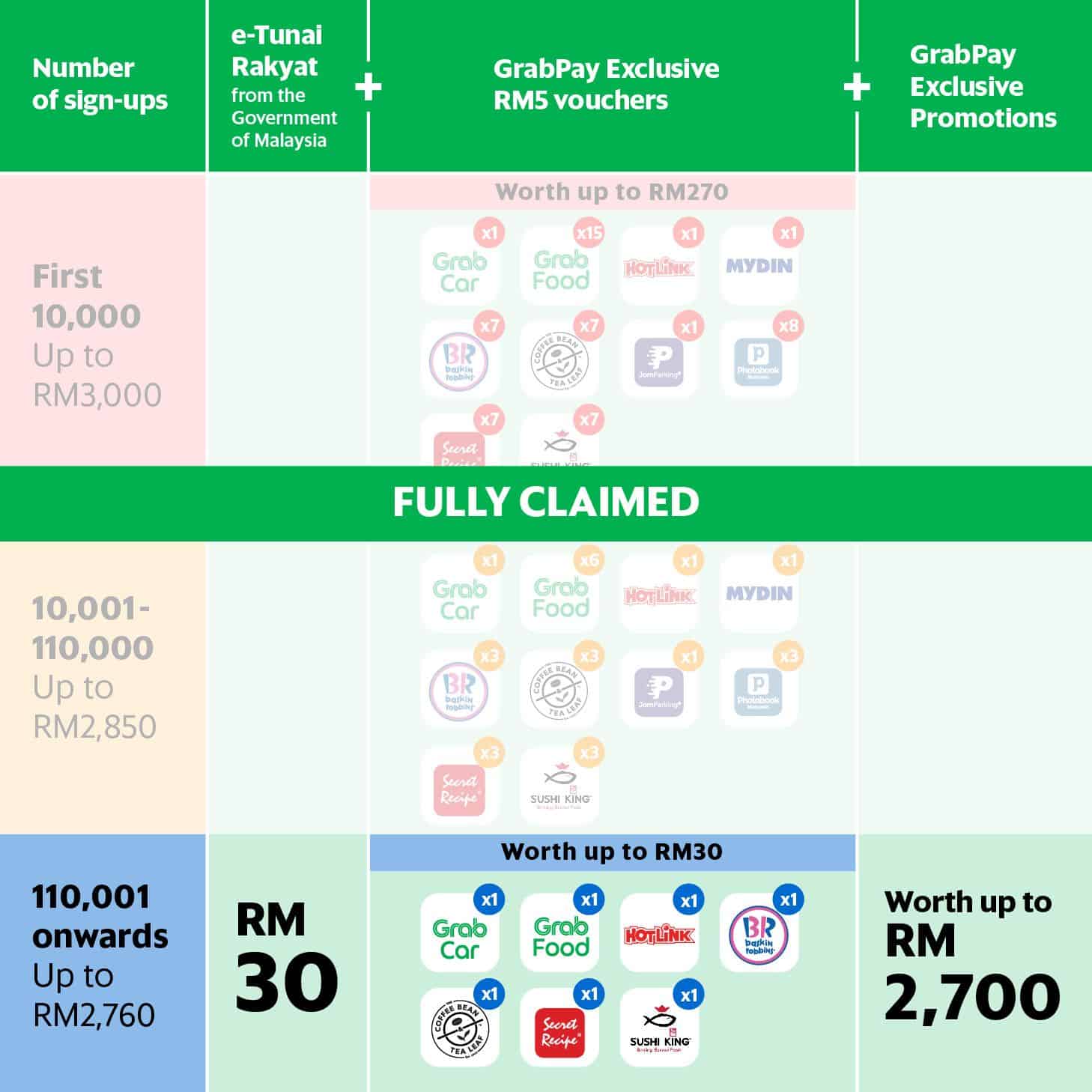

From 15 January 2020 to 8 March 2020, every eligible Malaysian can redeem RM30 from the government! Excellent news! However, with 3 distribution platforms – GrabPay, Boost and Touch N Go and each offering different promotions, how do you know which one offers the best bang for your bucks? You won’t go wrong with any, given they are all widely accepted. See my analysis below:

Touch ‘n Go

Getting RM60 in total sounds like a good deal. However, the blunder of TnG not coping with the initial volume probably have sent most users to other platforms.

If you’re not eligible for the RM30 voucher, fret not, TnG has something for you! See below!

Let’s hope I’m the first ONE million

Boost

Not gonna lie, Boost is looking good with all these attractive offers & games

RM 8,888 is hella sexy. However, if there is only one reward, with 5 million Malaysians on the platform, 1/5,000,000 sounds nil. I’d assume the expected value is 0 in this case. I am guessing most distributions would be at the lower end of <RM1.

UPDATE: Similarly as TnG, Boost offers a free shake for those who applied through the platform despite being ineligible for the offer.

The Ang Pows offer up to RM10 if you’re in it for a day. To continue the challenge, you gotta send one of the Ang Pows to another friend who is not already in the challenge. The circle will quickly become saturated in that case.

Boost is doing something right by offering a promo code to also encourage people to adopt this platform

My referral code is cin29ds2 if anyone is interested 🙂

GrabPay

Uh Oh I’m kinda late in writing this. THE BEST DEALS ARE ALL GONE!

Grab is really good at creating the sense of urgency, but if you look at what is being offered, it is actually worse than TnG. You have to spend money at the specific vendors to actually redeem the vouchers. If you frequent the said vendors, good for you. Otherwise, I’d say TnG gives you better value.

All in all, I’d rank them in the following order in terms of reward :

Boost

TnG Wallet

GrabPay

I personally went with TnG for its simplicity. You only have to spend at one of its 120,000 vendors to qualify for the extra RM30 cash back. (Source) While Boost might give you potentially higher return, it relies on the game of chance and requires you to actually spend time doing the challenges.

Do you agree with the ranking? Let me know what you think!

In my previous post, I briefly mentioned about time value of money and opportunity cost. Today, I am going to focus on opportunity cost. From a numerical perspective, it is easy to define what cost is – essentially the price you pay in exchange for something. What about value? How do you stick a number to value? How do you define opportunity cost in that transaction? There are a few ways to think about it.

Hourly wage

This is applicable to any salaried employees, just like myself.

To calculate your hourly wage, it is as simple as taking your net income per month (including EPF contribution through employer) and dividing it by the number of hours you work, or are at work. Illustratively, If I make RM5,600 a month net and I spend 160 hour a month at work, my hourly wage is RM35/hour.

It sounds little isn’t it? Every day I spend about 1/3 of my day at work, and potentially longer if I include the hypothetical commute time of 2 hours – the proportion of time I spend at work is closer to 42%. If I include the commute time in my calculation, my hourly wage is even lower – now it is RM31/hour.

Now, instead of looking merely at a price tag and the “I can afford it” mentality, try to look at every service or product you are trying to purchase – how many hours of work in exchange for that? If you hate every working hour with a passion, this metric should help you in evaluating your decisions.

Interest foregone/accrued

This is a FIRE/personal finance favourite, easily illustrated by the following scenario, or the well known “latte effect”. Starbucks is often the victim example, but given the climate in Malaysia, I will replace it with “bubble tea effect”.

A cup of bubble tea now is approaching RM12/cup. If you get a cup of RM12 bubble tea a week (hopefully sugar free), 52 weeks x 12 = RM624/year. Let’s say if you invest the money at a 6% per annum interest (624 x 1.06^20), you’re actually forgoing RM2,000 instead of RM624 in the bubble tea drinking habit.

Another crucial example is interest accrued on debt or credit. If you have RM1,000 right now and you have a credit card debt of RM1,000 running at an interest p.a. of 18%, ALWAYS pay the credit bill first, unless investing the money returns you a guaranteed interest of 20%. Doesn’t sound realistic? That’s why paying credit card comes first.

Cost per use and resale value

The reason why we buy something is that we expect to derive value out of it, but what is the right price to pay? You can tackle it by considering the cost per use. If a game is RM60 and you obtain an enjoyable experience of 60 hour, the cost for such entertainment is only RM1. While the ‘value’ that one can derive from such activity varies from person to person (and the opportunity cost for spending time on such events), you can use such method to evaluate the purchase.

Another thing to take into consideration is resale value. Just go on any second hand market place such as Carousell, mudah, lelong etc. to know what prices some of the second hand items fetch. For instance, Myvi has a better resale value than Axia of the same mileage and the depreciation is not as drastic. From anecdotal personal experience, stuff like clothes and books have almost nil resell value. Think extra hard about the utility of such purchase. I mostly end up just donating my books to the library and I swear by ebooks now.

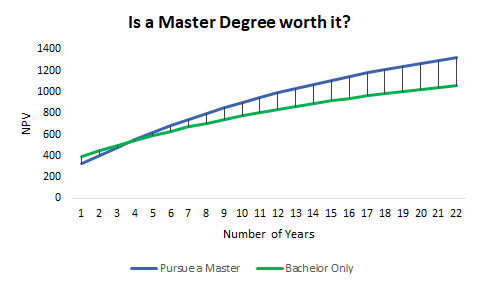

IRR/NPV

In corporate finance, evaluating business opportunities using the Internal Rate of Return (“IRR”) and Net Present Value (“NPV”) is a common practice. NPV is a more preferred method for a number of reasons which I will leave out. If you’re interested, the great web has a plethora of sources that will explain the intricacies to you.

Using the NPV method is beneficial as it incorporates the following elements: timing of cash flows, be it negative or positive, and time value of money or cost of capital. If the NPV is positive, the project is worth pursuing; and if not, you get the gist. While your prediction may not be 100% accurate, it gives you a good way to think about pursuing certain projects and how you should allocate resources.

I will give an example, and you can find the worksheet for this exercise here.

NPV worksheet – to pursue a master’s degree or not (Link)

Let’s say I want to pursue a master degree in data science in an American university. Room and board, and course fees are about USD80k a year. I am forgoing a year’s worth of salary, USD80k to pursue this degree but I expect that I can get an incremental USD40k per year for 5 years. Should I pursue this option?

Graph from Excel file

Based on the model, it takes about 4 years for that to happen. Whether it is worth it or not, it depends on you. The model is simplistic, but you can play around with the assumptions.

There are other capital budgeting methods such as breakeven period, but NPV trumps them all.

That’s all from me this week. I’m trying to keep up a posting frequency of once per week so do stay tuned!

Everyone budgets differently, and I’m no different. Here’s how I do it, month-in, month-out.

It consists of 3 parts.

Planning the month

Recording and categorizing daily transactions

Creating birds-eye views of finances

Planning the month

Every month, I divvy up my expected income into spending and savings categories. I give myself a spending buffer for flexibility. The category breakdown looks something like this:

paycheck

savings

investment account - retirement

investment account - non retirement

savings account

expenses

home

rent

insurance

bills

transportation

food

groceries

restaurants

office food

subscriptions

music

gym

discretionary

books

electronics

clothing

bars

shopping

gifts

travel

transportation

accommodation

food

entertainment

shopping

Recording and categorizing daily transactions

Throughout the month, I use a mobile app to manually record and categorize transactions. I prefer this over using automated tools that pull in transactions from your bank account, because the data usually needs to be manually cleaned anyway. It’s not too tedious, as long as the app you use is designed to make manual input easy. For now, that app is EveryDollar.

Creating birds-eye views of finances

At the end of the month, I tally up my totals, and move them to a spreadsheet with monthly data. It looks something like this:

Jan 2019

Feb 2019

March 2019

April 2019

paycheck

savings

investment account – retirement

investment account – non-retirement

savings account

expenses

home

rent

insurance

…

This allows me to see a birds-eye view of my monthly activity, in a way that I haven’t found in any free app. I can easily see what happened in any given month, and compare against any other month. It’s really neat when you start to accumulate years of this stuff. It starts to become a sort of outline of your life, where you can identify special events, and the start and end of eras.

I also have another spreadsheet that aggregates my annual activity. It’s probably more impactful because it underscores how little things add up, whether its expenses or savings. $100/month becomes $1200/year, and with a few more $100/month expenses easily becomes thousands a year. The money decisions that really matter are very clear when you look at the yearly totals. It’s a useful way to validate your decision making.

And that’s really it. I find that keeping track of where the money goes is enough to goad me into making more responsible financial decisions, especially when I can quickly see the big picture impact of those decisions. I get a real sense of what changes I actually want to make by gauging the amount of pain I incur by looking at certain numbers.